The decision to open a joint bank account might not be as straightforward as you think. There are a variety of benefits and risks associated with joint bank accounts that all involved individuals should weigh before opening a new account.

Who Should Open a Joint Banking Account?

Joint accounts offer a new level of convenience and flexibility for the account holders that weren’t possible before. Many joint banking accounts are started by couples who move in together, get engaged, or are married. The sharing of a bank account is a big step for most relationships as it combines financials together and forces partners to manage money with another person’s perspective in mind.

Joint banking accounts can also be a great solution for helping someone manage their own money. Parents will often set up joint accounts with their children as they enter their teenage years in an effort to help teach healthy financial habits and money management. These same accounts are also helpful for individuals with aging parents who may need additional help overseeing their finances.

Another common reason for starting a joint bank account is for business partners to have equal insight and responsibility for the related finances. Entrepreneurs and business owners often have co-owners or other stakeholders who need access to banking information and funds for day-to-day operations to run smoothly.

The Benefits of a Joint Bank Account

- Convenience: The biggest benefit and most commonly cited reason for opening a joint banking account is the convenience it affords multiple individuals when managing combined financials. Now all involved parties have equal visibility and responsibility for the management of their money. This helps co-owners pay for joint expenses easier, increase their buying power, and more.

- Increased FDIC Insurance: Combined accounts ensure each co-owner is listed on the account, increasing the amount of money covered by the FDIC. For example, a joint banking account held by you and your spouse would be FDIC insured for up to $500,000 — which is double what an individual bank account is covered for.

The Risks of a Joint Bank Account

- Financial Disagreement: Everyone has their own idea of how to best manage finances. This also leads to every individual having a different relationship with money. Joint banking accounts can cause disagreements and strife between account holders if they cannot agree on a middle ground strategy.

- Lack of Privacy: Due to multiple people having access to the account, all account co-owners can see financial history and actions, such as payments, withdrawals, and balances. This level of transparency can make it hard for some account owners who wish to not have every banking action be able to be scrutinized or questioned.

- Equal Responsibility: A joint banking account puts all co-owners on the hook for any overdrafts or issues associated with the account. This means the account assets are open for seizing to creditors, liens, and lawsuits if other co-owners get into financial or legal troubles.

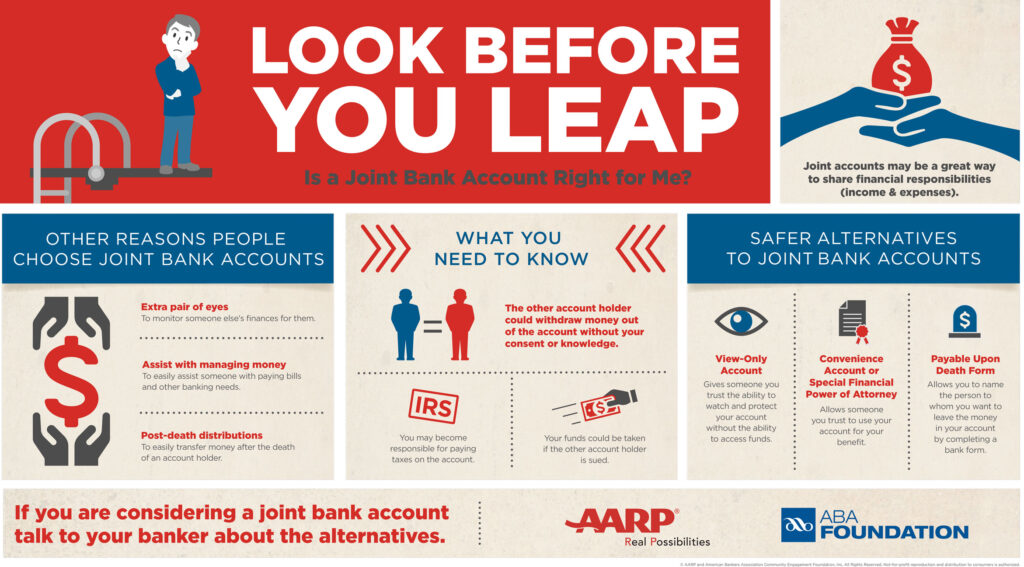

The American Bankers Association Foundation and AARP have produced an infographic to help people understand the risks of joint bank accounts.